How to Save Money on Therapy: Tips and Strategies

I know firsthand that it can be a big financial commitment. But the truth is, investing in therapy is an investment in yourself and your mental health. However, that doesn't mean you have to break the bank to get the help you need. In this post, I'll be sharing some tips and tricks for saving money on therapy, so you can prioritize your mental health without sacrificing your financial well-being. Let's dive in!

Before we dive into tips, let’s clarify what some of these terms mean ↓

Understanding Common Insurance and Therapy Terms

Out of Network/Private Pay

When a therapist is not part of your insurance company's network, meaning they may not be covered by your insurance plan or may have different coverage amounts.

In Network

Therapists who have contracted with an insurance company to provide services to its members. If you have insurance that covers therapy, you can usually see an in-network therapist for a lower cost than an out-of-network therapist.

Claims

A formal request to your insurance company for payment for a covered expense.

Deductible

The amount of money you must pay out of pocket before insurance coverage begins.

Copay

A fixed amount you pay for a covered service, such as a therapy session

HSA/FSA

Health Savings Accounts and Flexible Spending Accounts are pre-tax savings accounts that can be used to pay for medical expenses, including therapy.

Sliding scale

A payment structure in which the cost of therapy is based on your income and ability to pay, with lower fees for those with lower incomes.

Out of Network Vs. In Network Therapists

Finding an In Network Therapist

In-network therapists have contracts with insurance companies, which means that they have agreed to charge a certain fee for their services. This fee is typically lower than what you would pay for an out-of-network therapist.

If you have insurance and want to work with an in-network therapist, the first step is to check your insurance company's website or call their customer service line to find a list of in-network providers.

You can also ask your primary care doctor or a mental health professional for a referral to an in-network therapist. It's important to note that even with insurance, you may still be responsible for a copay or deductible when you see an in-network therapist.

Your relationship with your therapist is one of the biggest predictors of success in therapy, and working with someone who you truly click with can make all the difference.

But What if I Find My Dream Therapist and They’re Out of Network?!

Keep on reading, it’s not necessarily a dealbreaker.

Tips for Saving Money with Out Of Network/Private Pay Therapists

1. Check your out-of-network benefits

(PSST- You may still get a good amount of the therapy cost covered!)

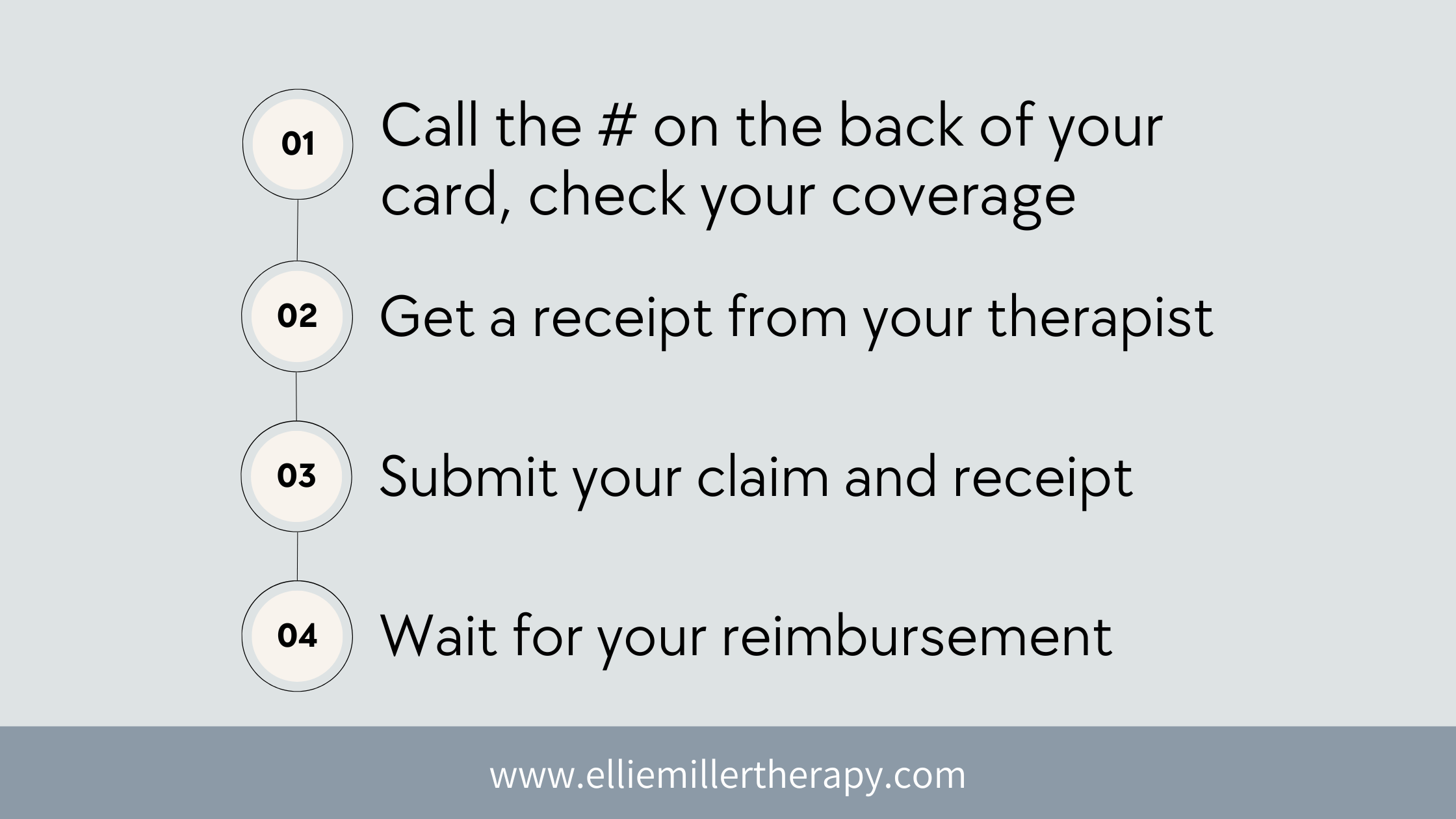

Call your insurance provider (the number on the back of your card) to confirm the coverage and the reimbursement rate. Ask how much out of network coverage you have for therapy.

Ask about any deductible, co-pay, or co-insurance that applies to out-of-network therapy.

The range for out-of-network mental health coverage can vary widely depending on the individual's insurance plan. Some plans may cover as little as 20% of out-of-network costs, while others may cover up to 80% or more. It's important to check with your insurance provider to understand your specific coverage and any associated costs.

2. Check your Health Savings Account (HSA) or Flexible Spending Account (FSA):

Determine if your HSA or FSA covers out-of-network therapy (it usually does).

Check if there are any restrictions or requirements for using the funds.

Keep receipts and documentation of payments for reimbursement.

3. Understand how using out-of-network coverage works:

Pay for therapy upfront and in full.

Submit a claim to your insurance provider with the necessary documentation (your therapist will likely be able to email you a receipt).

Wait for reimbursement from your insurance provider.

4. Calculate the potential cost savings:

Determine the reimbursement rate for your out-of-network therapy.

Subtract the reimbursement rate from the therapist's fee to see your out-of-pocket cost.

Multiply your out-of-pocket cost by the number of therapy sessions per year to estimate annual expenses.

5. Submitting a claim for reimbursement:

Collect a receipt from your therapist for each session. As easy as getting a quick email from most therapists these days.

In my private practice I ask if clients would like me to either send them their receipt after each session or get the receipt monthly. It’s up to you!

Complete any necessary forms or paperwork from your insurance provider.

Submit the receipt and paperwork to your insurance provider for reimbursement.

Remember, it's important to do your research and talk to your insurance provider to understand your coverage and reimbursement options. While out-of-network therapy may require more effort and upfront costs, it could be a more affordable option in the long run.

6.) Get Help Submitting Claims: Programs to Ease the Process

Submitting claims for out-of-network therapy services can be a hassle, but fortunately there are programs that can help. Some programs, offer a service where they will submit your claims for you in exchange for a small fee. This can save you time and reduce the stress of dealing with insurance paperwork.

Here are some benefits of using these types of programs:

They’ll handle the paperwork for you, reducing the time and effort required on your part.

These programs can often negotiate with insurance providers to maximize your reimbursement.

You may be able to get reimbursed faster, as the program will typically have experience dealing with insurance providers and can help ensure that your claims are processed quickly.

They can offer guidance and support throughout the process, answering any questions you may have and helping to ensure that you get the most out of your insurance coverage.

Claim Submitting Services

Mentaya is a service that helps people get reimbursed for their out-of-network therapy sessions. They submit claims on behalf of their clients and charge a small fee for their services.

Better is a service that helps people get reimbursed for out-of-network medical expenses, including therapy sessions. They offer a streamlined process for submitting claims and charge a fee based on a percentage of the reimbursement amount.

Health Sherpa is a health insurance marketplace that also offers a service for submitting out-of-network claims for reimbursement. They charge a flat fee for their services and can help clients navigate the process of submitting claims and getting reimbursed.

Reimbursify is another service that helps people submit out-of-network therapy claims for reimbursement. They offer a user-friendly app for submitting claims and charge a flat fee for their services.

*It's worth noting that while these services can be helpful, they do charge a fee for their services, so it's important to weigh the costs and benefits of using them versus submitting claims on your own.

Affordable Alternatives to Out of Network Therapy

In Network Therapy

Group Therapy

A recap

Think of therapy as a long-term investment in your mental health and well-being. By taking care of yourself now, you'll be better equipped to handle challenges in the future.

Consider the cost of not getting therapy. Untreated mental health issues can have a negative impact on your relationships, work, and overall quality of life. Investing in therapy now can prevent these negative outcomes down the road.

Look for ways to make therapy more affordable. As we've discussed, there are options like using an HSA/FSA, checking for out-of-network coverage, and using reimbursement services like Mentaya. Some therapists may also offer sliding scale fees based on income.

Remember that you deserve to prioritize your mental health. Investing in yourself is never a waste of money.

It's important to note that seeking out a private-pay therapist is not the right choice for everyone. Some people may prefer to work with a therapist who accepts insurance, and that's completely valid.

The most important thing is finding a therapist who you feel comfortable working with and who can help you achieve your therapy goals, while not feeling like you’re breaking the bank.

Best of luck in your therapy search process!

Hi! I’m Ellie, a Baltimore based private practice therapist offering online therapy to empathetic women & couples in Maryland. I help women manage anxiety & stress and couples strengthen their relationships.

If you want more anxiety tools and tips from my private practice, straight to your inbox, I’d love to have you join The Detangler, my weekly lighthearted newsletter. If you live in Maryland or Virginia, reach out to see if we’re a good fit for therapy.